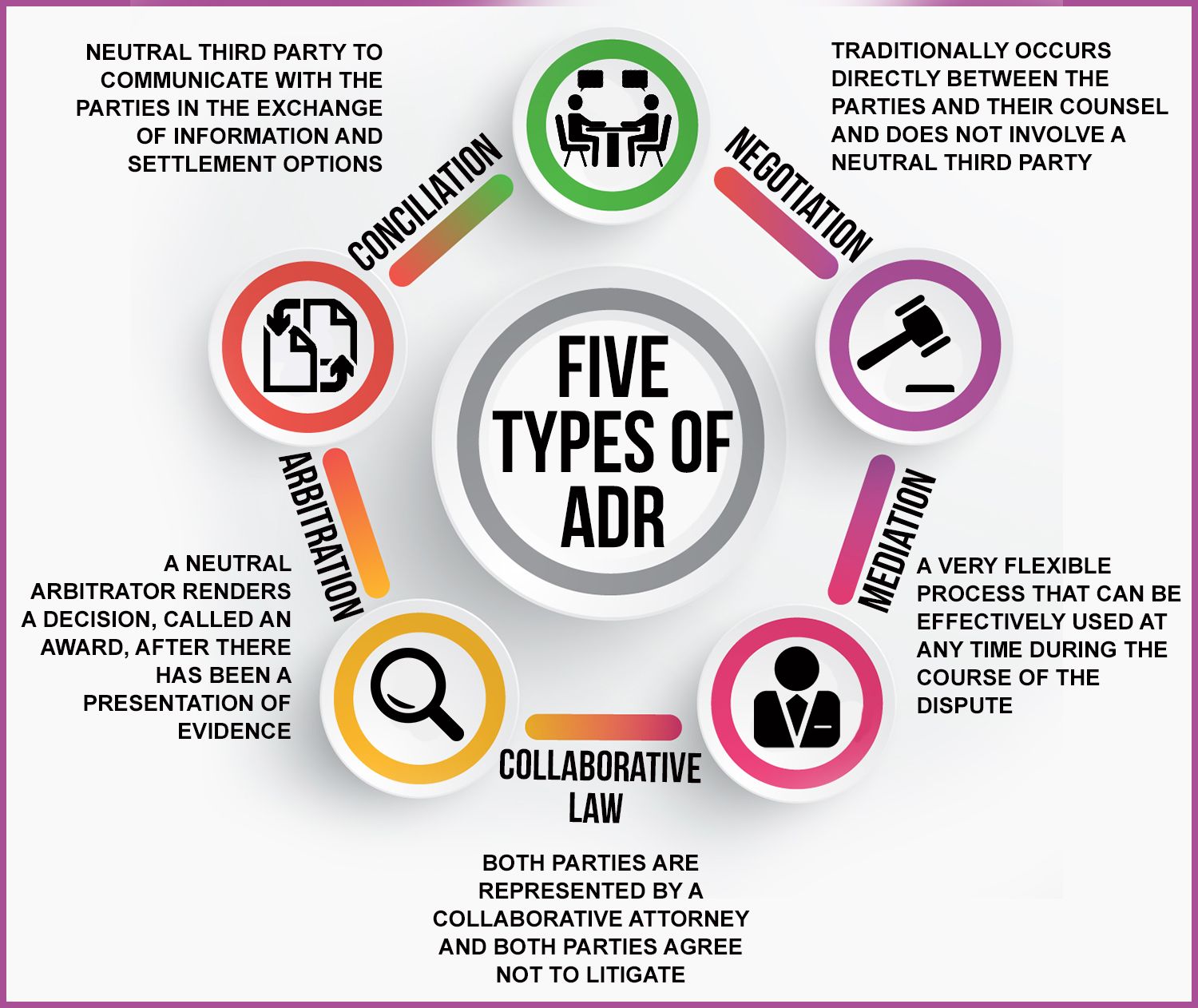

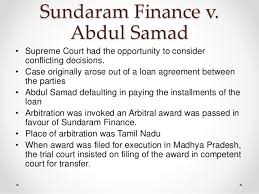

There are currently over 197 Islamic banks functioning in Indonesia, indicating a considerable evolution of the Islamic banking sector. Mudharabah finance arrangements, which are profit-sharing agreements that promote cooperative partnerships and reduce the chance of business bankruptcy, have become more prevalent as Islamic banking has grown. Nonetheless, disagreements about how money is distributed between banks and clients sometimes occur, especially when there are defaults or other problems. The most frequent cause of non-performance is the customer's incapacity to pay, which might cost the bank money. The Islamic Banking Law No. 21 of 2008 offers two methods for resolving these disputes: non-litigation through an out-of-court institution and litigation through a judicial institution. In contrast to discussion, consultation, mediation, and expert views, which offer answers without imposing a decision on the parties to the conflict, arbitration is a final and binding settlement that cannot be challenged or appealed. The author's goals are to examine BASYARNAS's standing as the greatest alternative to litigation for non-litigation dispute resolution and to examine how Islamic banking uses Mudharabah finance to resolve default problems. A statutory method based on legislative rules, such as Law No. 30 of 1999 addressing arbitration and alternative dispute resolution and Law No. 21 of 2008 about Islamic banking. Because arbitration has benefits over litigation, it is frequently selected in Islamic financial transactions. Islamic arbiter BASYARNAS is in charge of settling conflicts about Sharia banking as well as other Sharia-related issues, particularly those involving arbitration or hakam. Twenty Sharia-related financial disputes have been settled by BASYARNAS since its founding. With a strong legal basis in Indonesian law, the National Sharia Arbitration Council (BASYARNAS) is the sole Islamic arbitration organization in the country.

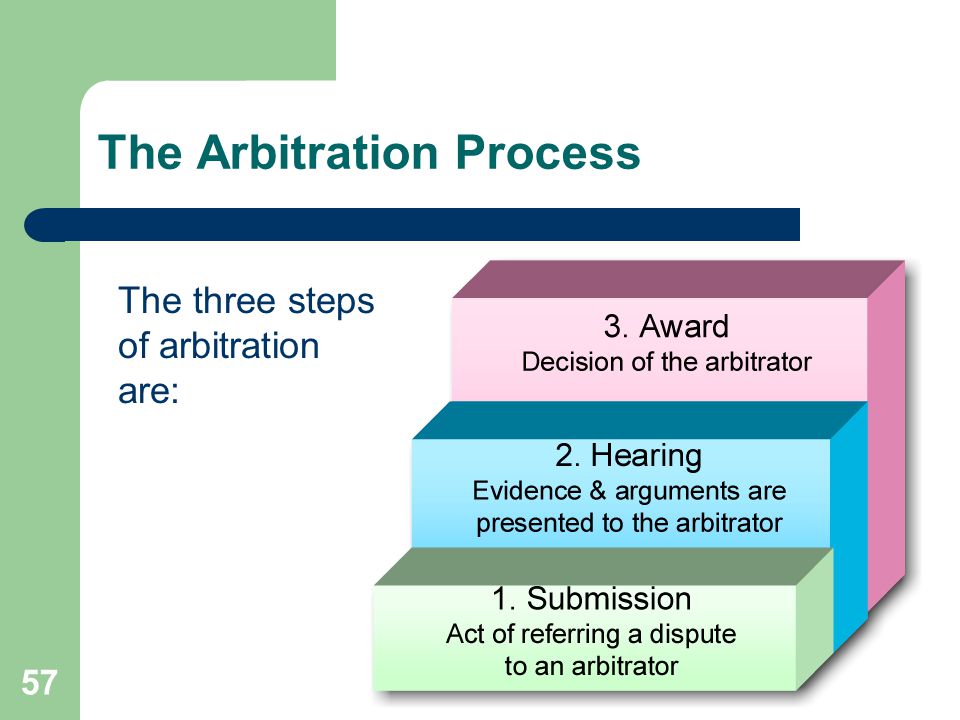

In Indonesia, parties to a disagreement can settle it outside of court by using an independent organization like BASYARNAS, which settles financial and banking conflicts by Sharia law. Parties in dispute must reconcile before beginning the secret arbitration process. Six months are allotted for resolving the conflict. The parties must willingly implement the judgment, and the enforcement of the decision is equivalent to that of the Indonesian National Arbitration Board (BANI). The Chief Justice is not permitted to review the decision, which is binding and final. In Islamic banking, maharajah financing is transferring funds to an email in exchange for trade and profit sharing. The Islamic Ulema Council and the Qur'an both provide explanations of the legal foundation for mudharabah. The consumer serves as mudharib (manager), and the bank as shahibul maal (owner of capital). The Mudharabah mullah and Mudharabah Muqayyadah term savings products from time deposits are the two categories to which the concept is applied.

In Islamic banking, mudharabah is a common type of musyarakah in which the manager (mudharib) has a profit-sharing contract and is the capital owner. This arrangement places a strong emphasis on collaboration and Mudharib and Shahib Almal's 100% cash capital participation. Mudharabah is a type of trust arrangement that requires justice and candor. The two phases of mudharabah implementation in Islamic banking are fund distribution and fund direction. Islamic banks provide profit-sharing deposit products called mudharabah savings and deposits, whereas mudharabah financing entails the bank providing complete funding for the project or business that the customer has suggested. A debtor may default for purposeful or careless reasons if they are unable to pay for a facility that has been promised. Legal ramifications for an individual's activities that may be deemed in default might result from negligence causes.

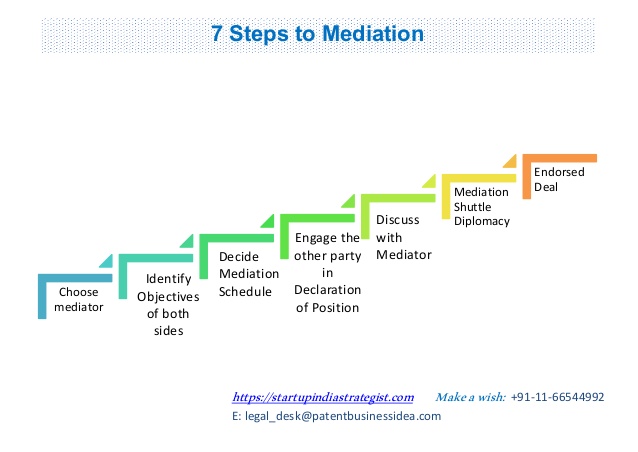

Islamic banking arrangements create a debtor-creditor relationship in which debtors are required to pay creditors what they owe. A party who fails to perform its duties owing to carelessness, incompetence, or willfulness is said to be in default in legal parlance. Default in Islamic banking can take many different forms: not fulfilling commitments, fulfilling promises but not as promised, maintaining pledges but after it's too late, or acting against the terms of the contract. Religious courts have the authority to settle matters about marriage, inheritance, wills, waqf, zakat, and the sharia economy. Disputes may be settled by litigation or non-litigation. A written agreement and arbitrators chosen by the parties provide the basis of arbitration, a process for settling civil disputes outside of public courts. It is regarded as an extrajudicial conflict settlement process that offers benefits including speedier resolution timeframes and secrecy. If disagreements on mudharabah funding are deemed defaults, the party that feels wronged may seek dispute resolution via the contract.

In Islamic banking, parties have the legal option to resolve default disputes in financing contracts to mend issues and reestablish commercial and legal relationships. The parties' agreed-upon agreement contract contains the rules governing dispute settlement. According to the Sharia Banking Law, the resolution of default claims in maharajah finance contracts must give priority to methods of dispute resolution that involve discussion and agreement. If the settlement fails, it may be possible to reach a new agreement outside of court by using BASYARNAS for dispute resolution. BASYARNAS is authorized by the agreement provision to arbitrate disputes on behalf of the parties. Losses in Maharajah finance must be absorbed without remuneration by the capital owner. Should the loss be the result of the client's carelessness, the client will be liable for the legal fees. The parties must register the arbitration ruling with the court to secure execution if required. The arbitration award is final and binding.