Latest News

AN OUTLOOK OF “VIVAD SE VISHWAS” BILL

AN OUTLOOK OF “VIVAD SE VISHWAS” BILL

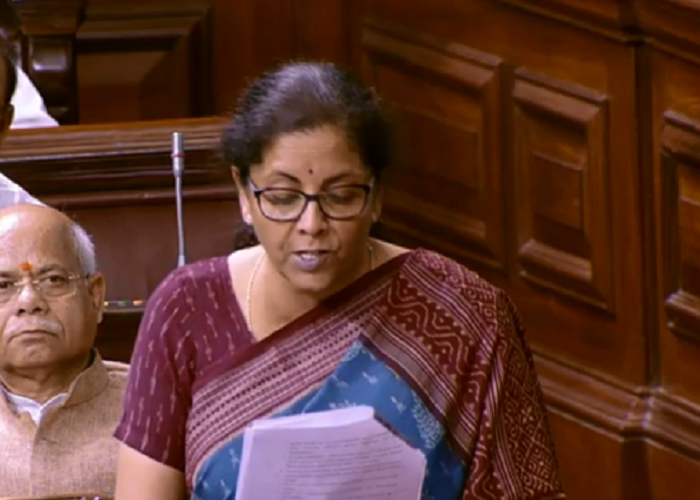

Inspired by the accomplishment of the Sabka Vishwas Scheme, which decreased several indirect tax disputes, the Finance Minister presented The Direct Tax Vivad se Vishwas Bill, 2020 in Parliament on February 5, 2020. Its key target is to collect taxes and at the same time reduce litigation. It offers a total waiver on interest and penalty to the taxpayers who pay their disputed taxes on or before March 31, 2020.

To extend the scope of the scheme, certain amendments to the Bill were proposed to the Parliament on February 14, 2020. The amended Bill was passed by the lower house of the Parliament on March 04, 2020 and from Upper house on March 13, 2020. Further, the legislature likewise gave FAQs to explain the provisions of the Bill and some practical perspectives. So as to become an Act it will require a further approval of President's consent.

Who is qualified to opt on the scheme?

The scheme shall be applicable to all the appeals/petitions filed by taxpayers or the income tax department, which are pending on January 31, 2020 with the accompanying discussions:

- Commissioner of Income-tax (Appeals);

- Income-tax Appellate Tribunal;

- High Court; or

- Supreme Court

Further, the scheme is additionally applicable to the following situations where, as on January 31, 2020:

- Time limit for filing an appeal has not terminated;

- Cases are pending before the Dispute Resolution Panel (DRP) or where DRP dealings have been passed but final assessment order is anticipated;

- Revision petitions are pending before the Commissioner of Income-tax; and

- Search cases where the disputed demand is not more than Rs 5 crore.

On the practical aspects, the FAQs issued by the government has explained that there are no provisions in the scheme to settle some portion of a pending dispute in relation to an appeal / petitions. The FAQs gave clarity on extent of the scheme, procedural perspectives, computational angles and consequential factors also.

What advantage the taxpayer gets, when the case is settled under the scheme?

Aside from waiver of interest and penalty, the taxpayer will likewise get the accompanying immunities once the case is settled under the scheme:

- Such cases can't be reopened in any other proceeding by any tax authority or designated authority;

- Once the dispute has been settled, an appellate forum cannot issue an order in relation to the issue; and

- Opting for the scheme shall not amount to conceding the tax position and tax authority cannot claim that taxpayer has acquiesced to the decision on the disputed issue.

Fundamentally, the scheme is the government's initiative to reduce disputes and furthermore collect the revenues clogged in long pending litigations. Every steps of government means show the eagerness of the government in contacting the taxpayer to empower settlement of long pending disputes. The Central Board of Direct Taxes (CBDT) has already stated advertising the scheme in leading newspapers and furthermore inside directed all revenue officials to take appropriate steps to ensure that taxpayers take the benefits available under the scheme and settle disputes.

In spite of the fact that these are steps in the right direction towards building taxpayers "Vishwas", implementation of the scheme may pose certain practical challenges given the cut off of March 31, 2020 is fast approaching. Remembering this, the government ought to consider extending this date with the goal that taxpayer have adequate time to avail the benefits of the scheme.

It may not be inappropriate to say that this is indeed a golden opportunity for taxpayers to resolve the disputes if they believe the litigation are not worth their time and efforts, and start evaluating their cases.

- The Finance Minister presented The Direct Tax Vivad se Vishwas Bill, 2020 in Parliament on February 5, 2020.

- To extend the scope of the scheme, certain amendments to the Bill were proposed to the Parliament on February 14, 2020.

- The amended Bill was passed by the lower house of the Parliament on March 04, 2020 and from Upper house on March 13, 2020.