Latest News

Steps for settling dispute complying with “Vivad Se Vishwash bill”

Steps for settling dispute complying with “Vivad Se Vishwash bill”

What is the process to settle the tax dispute under the scheme?

Under the tax dispute resolution scheme, an individual taxpayer has to complete the following steps by March 31, 2020, to avail the benefit of complete waiver of interest and penalty:

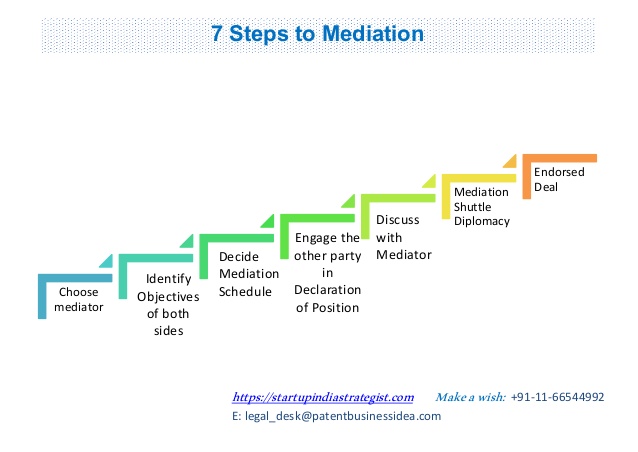

Step 1: Taxpayer has to file a declaration in a specified Form (which is yet to be notified) to the designated authority (Principal Chief Commissioner shall designate an officer, not below the rank of a Commissioner of Income-tax as the designated authority) to initiate resolution of pending direct tax disputes. Along with the declaration, the taxpayer has to also furnish an undertaking in a specified format (which is also yet to be notified) waiving his right to pursue any other remedy.

Step 2: Based on the declaration, within 15 days, the designated authority will determine the amount payable by the Applicant and grant a certificate, containing particulars of the amount payable. It has been clarified that the applicant will not be able to file an appeal in case it does not agree to the amount determined by the designated authority.

Step 3: The Applicant has to make the payment of the said amount within the next 15 days and submit the proof of withdrawal of the appeal. The proof of appeal could either be an order dismissing the appeal due to withdrawal or can be the application filed to withdraw the appeal.

Step 4: The designated tax authority will then pass an order, which shall be conclusive as to the matters stated therein.

However, in case the above four steps are not completed by March 31, 2020, then there will be an additional payment as discussed in the table above.

What is the amount payable in the scheme?

Under the scheme, taxpayers will be required to pay the following:

Appeals filed by the taxpayer:

- Search cases

On or before 31st march 2020 – 125% of disputed tax

Post 31st March 2020 – 135% of disputed tax

- Other than search cases

On or before 31st march 2020 – 100% of disputed tax

Post 31st March 2020 – 110% of disputed tax

- Cases related to interest, penalty, and levy

On or before 31st march 2020 – 100% of disputed tax

Post 31st March 2020 – 110% of disputed tax

Appeals filed by Department or the Department has lost an issue

- Search cases

On or before 31st march 2020 – 62.5% of disputed tax

Post 31st March 2020 – 67.5% of disputed tax

- Other than search cases

On or before 31st march 2020 – 50% of disputed tax

Post 31st March 2020 – 55% of disputed tax

- Cases related to interest, penalty, and levy

On or before 31st march 2020 – 12.5% of disputed tax

Post 31st March 2020 – 15% of disputed tax

Disputed tax, in relation to an assessment year, is essentially a tax on disputed income.

Further, it has been clarified that if the taxpayer has already paid the disputed demand which is more than the amount payable under the scheme, the taxpayer shall be entitled to refund (but without interest on the refund due).

- What is the process to settle the tax dispute under the scheme?

- What is the amount payable in the scheme?

- Further, it has been clarified that if the taxpayer has already paid the disputed demand which is more than the amount payable under the scheme, the taxpayer shall be entitled to refund.